WORLD - For decades, economists measured the health of the global economy through a familiar set of indicators: capital stock, labor supply, trade openness, and productivity gains derived from the interplay between the two core factors of production. These principles offered a reliable, if imperfect, way of understanding where growth came from. That understanding is now being tested.

The past decade has subjected the global economy to a sequence of compounding disruptions: a pandemic that restructured markets overnight, trade tensions that exposed the fragility of integrated supply chains, climate shocks that repriced risk across entire sectors, and a geopolitical realignment that has challenged the assumptions underpinning post-Cold War economic integration. Taken together, these forces have not merely slowed growth; they have altered its underlying conditions.

Technology has deepened this structural shift. The rapid advancement of artificial intelligence is redefining both labour and capital, changing how productivity is generated, who generates it, and which assets command value in a modern economy. The traditional factors of production have not disappeared, but the equation has changed.

A report published in April 2026 by the World Economic Forum, Growth in the New Economy: Towards a Blueprint, formalizes what many economists have been observing: old growth strategies are unlikely to yield returns in the new economy. Drawing on IMF projections and a survey of over 11,000 business executives across more than 100 countries, the report argues that the new economy demands a flexible blueprint, one that accounts simultaneously for technological disruption, climate imperatives, mounting debt, and geopolitical fragmentation

The Geography of Growth is Shifting

Alongside these structural changes, the geographic distribution of economic activity is changing. The WEF report projects that middle-income economies will account for 65% of cumulative global GDP growth between 2025 and 2030, a significant shift from the concentration of output that defined the advanced-economy era. Asia alone is expected to contribute approximately 50% of global growth over the same period, reflecting the continued rise of emerging economies and regional blocs as primary engines of expansion. By contrast, low-income economies, despite recording the fastest growth rates at 7.4% annually, are projected to represent just 1% of global growth.

What these projections signal is not simply a transfer of growth from one set of countries to another. They suggest a reformulation of the conditions under which economies grow.

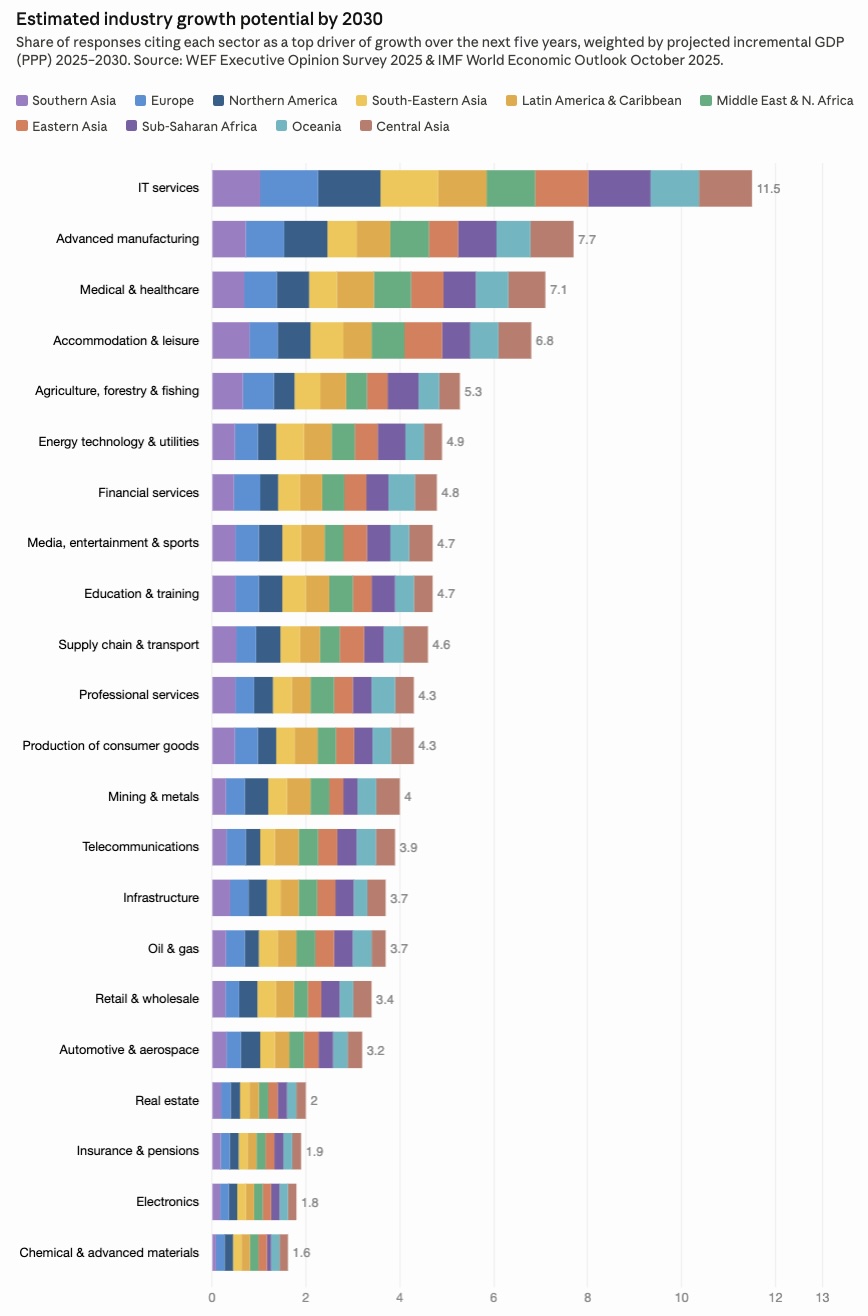

Industries in the New Economy: Key Growth Sectors

Not all sectors are equally positioned to benefit from the structural shifts reshaping the global economy. Based on IMF GDP projections combined with responses from over 11,000 business executives surveyed by the World Economic Forum, a clear picture of growth potential emerges across industries through 2030.

What the data shows

Information technology (IT) services ranks as the single most important driver of expected economic growth, with a weighted score of 11.5 out of 100, well ahead of every other sector. This reflects the degree to which digital transformation has become a cross-cutting factor in every industry: IT services drive productivity gains in manufacturing, finance, healthcare, and trade simultaneously, giving it a structural importance that other sectors do not share.

Advanced manufacturing (7.7), healthcare (7.1), and accommodation and leisure (6.8) each demonstrate strong growth potential, combining industrial upgrading with the continued shift toward service-based economies shaped by demographic change and evolving consumer behavior. Agriculture (5.3) and a cluster of mid-ranking sectors including energy, financial services, and media each score in the 4.7 to 4.9 range, pointing to moderate but steady expansion.

At the lower end, traditionally important sectors such as real estate (2.0), electronics (1.8), and chemicals and advanced materials (1.6) are among the least cited as growth drivers.

Looking Ahead

The shifts outlined in this report are not temporary changes. The rebalancing of growth toward middle-income economies, the rise of IT services and knowledge-intensive industries, and the shrinking role of traditional capital-intensive sectors all point to a structural reconfiguration of how and where economic value is created.

For economies at different stages of development, the implications are significant. Growth in the new economy rewards digital infrastructure, human capital, and institutional adaptability over natural resources and manufacturing scale. How countries move from low-income to high-income status is changing. The new economy does not come with a ready-made model. What it asks of governments and businesses is the ability to build their own, and to keep building as conditions change.